BIC and SWIFT codes identify banks and financial institutions in international transactions and ensure payments are processed securely and efficiently. As a UK resident, whether or not you’ll need to use a BIC/SWIFT code will depend on where you’re sending your money. If you’re sending your money:

Within the Single Euro Payments Area (SEPA): You probably won’t need a BIC/SWIFT code to make the transfer. Since 2016, BIC/SWIFT codes haven’t been compulsory as long as you can provide your International Bank Account Number (IBAN) for international transactions within the SEPA network.1

Transfers to non-SEPA countries: Many countries outside the SEPA network require an IBAN and a BIC/SWIFT code for international transfers. If you want to search whether the country you are transferring to uses BIC/SWIFT codes, you can check on the Swift website.

In this guide, we’ll cover information about BIC/SWIFT codes so that if you ever have to use them, you have an understanding of what they are and how they work.

Are BIC and SWIFT codes the Same?

The short answer is yes. Both terms refer to the same banking identifier (BIC), which the SWIFT network assigns to financial institutions, like banks, worldwide. This is why the two terms are often used interchangeably.

- BIC – Stands for (Bank Identifier Code) and is used to identify a specific bank during international transactions 2

- SWIFT Code – Provides the same role as a BIC but is named after the system that issues them: the ‘Society for Worldwide Interbank Financial Telecommunication’ 3

Regardless of the term used, a BIC or SWIFT code ensures that when you transfer money abroad, your money reaches the right bank securely and efficiently.

BIC vs SWIFT codes

What is a BIC Code?

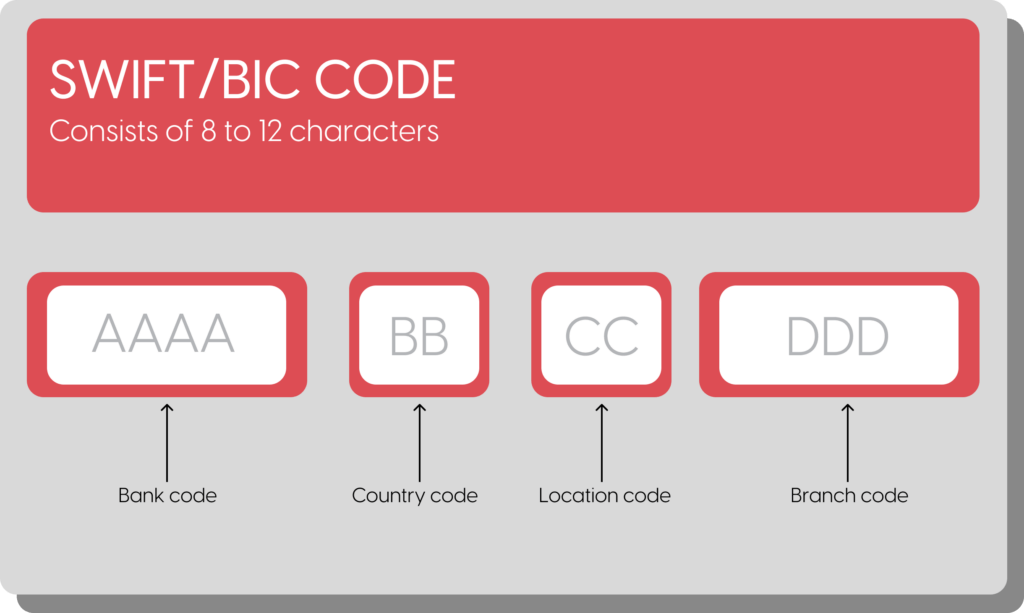

A BIC code is an internationally recognised bank identifier code that helps financial institutions process transactions securely and accurately. It consists of 8 to 11 characters and provides details about the bank, its country and its location.2

Here’s a BIC code example: Barclays Bank UK (BARCGB22XXX)

Each part of the code is used to identify a different part of the bank:

- BARC – Barclays Bank

- GB – United Kingdom

- 22 – London headquarters

- XXX – Branch code

So, if you need to send payments internationally, the BIC code ensures that your money is directed to the correct institution.

What is a SWIFT code?

SWIFT stands for the ‘Society for Worldwide Interbank Financial Telecommunications’ and refers to a network connecting over 11,000 banks in more than 200 countries.3

So, while SWIFT codes also identify a specific bank or financial institution in global transactions, its name refers to the network of banks rather than the individual bank identification code.

You can find the complete list of countries in the SWIFT network on the SWIFT’s official website.

Do All Countries Use BIC/SWIFT Codes?

While SWIFT is widely used, it’s important to know that some countries rely on alternative systems:

- U.S. – CHIPS (Clearing House Interbank Payments System)4

- China – CIPS (Cross-Border Interbank Payment System)5

- Russia – SPFS (System for Transfer of Financial Messages)6

New technologies like blockchain and the ISO 20022 also aim to enhance cross-border payments.7 However, SWIFT remains the most popular option due to its widespread adoption.

BIC/SWIFT vs. IBAN: What’s the Difference?

Whenever you make any type of cross-border transfer, you’ll need to identify the IBAN (International Bank Account Number). Put simply, this number identifies the specific bank account you’re sending money to.8

The BIC/SWIFT code does not identify the specific account but identifies the bank receiving the funds. Since you’ll always need to identify the bank and the specific account to make an international transfer, you’ll need both an IBAN and BIC/SWIFT code to complete a payment overseas if it is to a country outside of the SEPA network.8

What are BIC/SWIFT codes used for?

International wire transfers

A ‘wire transfer’ differs from a standard bank transfer because it moves money directly between banks using a secure network, making it faster and irreversible. This makes SWIFT/BIC code transfers different from other international transfer networks like the Single Euro Payments Area (SEPA), which rely on standard transfers and need to go through clearing systems, adding a few more steps to the process.

Foreign exchange transactions

SWIFT transfers are regularly used for foreign exchange because they create a standardised system and a secure way to send money internationally between banks in different countries.

In other words, the SWIFT network connects banks worldwide, allowing them to exchange currency and settle payments securely using unique SWIFT codes.

Business-to-business (B2B) payments

Since SWIFT transfers enable fast, reliable and traceable cross-border payments, they are also a great option for businesses sending money internationally.

How BIC/SWIFT codes work on international transfers

While Lumon does ask for BIC/SWIFT codes to make an international transfer, an IBAN could be sufficient depending on the country you are sending your funds to. In countries that don’t use IBAN, a BIC/SWIFT code will be essential to make the transfer. Here’s how a BIC/SWIFT code is then used in your international transfer:

- You initiate a transfer – As the sender, you provide the recipient’s IBAN and BIC/SWIFT code.

- The sending bank processes the request – Your bank transmits a payment message through the SWIFT network to the recipient’s bank.

- Intermediary banks handle routing – If a direct relationship doesn’t exist between the sender’s and recipient’s banks, intermediary banks may facilitate the transaction.

- The recipient’s bank receives the funds – The money is deposited into the correct account as the recipient’s bank receives the SWIFT message

Security with BIC and SWIFT transfers

What makes BIC/SWIFT transactions so secure?

BIC and SWIFT transactions are renowned for their robust security, ensuring safe and reliable financial communications across the globe. The security of these transactions is underpinned by a few key features.

- Unique Identification with BIC: A BIC code acts like a unique fingerprint for banks and financial institutions worldwide. It clearly identifies each bank, ensuring that all money transfers go to the right place, reducing mistakes and lowering the risk of fraud.2

- Advanced encryption and authentication with SWIFT: ‘Encryption’ is a way to protect customer transactions both during transmission and while ‘at rest’ in SWIFT systems. Encryption is a way to turn your message, which will hold details of your money transfer, into a secret code so it can’t be altered or intercepted by unauthorised parties.3

The SWIFT network is subject to regular compliance checks and audits to ensure they adhere to stringent data security standards in line with SWIFT’s data protection policies.

Common pitfalls when using BIC/SWIFT Codes

While Lumon does ask for BIC/SWIFT codes to make international transfers, an IBAN could be sufficient depending on the country you are sending your funds to. In countries that don’t use IBAN, a BIC/SWIFT code will be essential to make the transfer.

In the case you need to provide a BIC/SWIFT code, here are some common mistakes you can avoid:

- Always verify the correct BIC/SWIFT code: Using the wrong code can mean the money doesn’t reach your destination.

- Banks occasionally change their codes: Try and check whether the codes are still in date

- You might need intermediary bank details: For certain transactions, these are needed.

- Both IBAN and SWIFT/BIC codes are required: Sometimes, people think IBAN and SWIFT/BIC codes can be used as substitutes for each other. Both IBAN and SWIFT/BIC will be needed for international transfers and serve two different roles in the transfer process.

FAQs

Is a SWIFT code the same as an IBAN?

No. SWIFT codes are used to identify the bank, while an IBAN identifies the specific bank account within it. Both serve separate roles during international transfers, and both are required when you are looking to move money overseas.8

Do all bank branches have unique BIC codes?

Not all bank branches have unique BIC codes. The BIC code used varies by the institution using it:8

- Single BIC code for all branches: Some banks choose to use one SWIFT code for all of their bank branches.

- Unique BIC codes for each branch: Other banks choose to assign specific SWIFT codes to individual branches. Especially if the banks are larger and have many locations, SWIFT codes can be used to differentiate between their different bank branches.

How can I find my BIC/SWIFT code?

There are a couple of places you can find your BIC/SWIFT code.

- Try Online Banking: If you use online banking, you can find the BIC/SWIFT code in the ‘account details’ section.

- Use your IBAN: Alternatively, you can use tools such as this IBAN Calculator to validate your IBAN and get your SWIFT/BIC.

Can I make a transfer without a BIC/SWIFT code?

Whether you need to make a transfer with a BIC/SWIFT code depends on your transfer destination and specific banking requirements. If your transfer is within the Single Euro Payment Area (SEPA), providing the IBAN is usually sufficient.1

However, when sending money to countries outside of the SEPA network ((including non-SEPA European countries and non-EEA countries), you may need both an IBAN and a BIC/SWIFT code. If you would like to search whether or not the country you are transferring to uses BIC/SWIFT codes, you can check on the Swift website.

How long do BIC/SWIFT transfers take?

While BIC/SWIFT transfers typically take between 1 and 5 business days to complete, this timeframe depends on several factors, such as the countries involved, intermediary banks, and the processing times of the banks handling the transfer. It’s always best to check with your bank for precise timelines, as overseas payments may take longer.

We’re here to help

At Lumon, we make cross-border transfers simple and efficient. Our dedicated currency specialists are here to guide you through our range of solutions designed to help you lock in a bank beating exchange rate.

Better rates than the high-street banks*

Get more euros for your money when you transfer £50,000 with Lumon.

*This chart is intended to represent the range of euro outcomes a consumer may achieve on a £50,000 transfer of pounds to euros, inclusive of fees and charges. Comparison data for the high-street banks is from FXC Intelligence (FXC Intelligence | Payments Market Data for Global Payments). Comparison data for the high-street banks utilises pricing data provided under licence from FXC Intelligence (FXC Intelligence | Payments Market Data for Global Payments), a specialist benchmarking tool, for transactions in March 2026. The Lumon rate is calculated by taking the GBPEUR spot rate from 2 March 2026 from the Bank of England (bankofengland.co.uk) and then applying the median FX cost percentage across 69 spot GBP to EUR transactions with a value in the range of £25,000-£50,000 performed by Lumon Pay Limited and associated Group Companies (Lumon Risk Management Limited, Lumon FX Europe Limited) for personal customers during March 2026. Please note the amounts above are based on data from March 2026, so do not reflect live dealing rates.

Sources used:

1 European Union – Regulation (EU) No 260/2012

2 Swift – Business Identifier Code (BIC)

3 Swift – Compliance, Swift & Sanctions

4 The Clearing house – CHIPS

5 CIPS, Cross-Border Interbank Payment System – About us

6 Bank of Russia – Financial Messaging System of the Bank of Russia

7 Swift – ISO 20022 for Financial Institutions: Focus on Payments instructions

8 Swift – International Bank Account Number (IBAN)

Sources last checked on date: (06/03/2025)

The information provided in this material is accurate to the best of our knowledge at the time of writing (06/03/2025), but it is subject to change. The content is for informational purposes only and does not constitute advice. It is essential that individuals seek advice from professional services regarding tax matters. We do not accept liability for any errors or outdated information, and individuals should not rely on the information presented without consulting an expert.