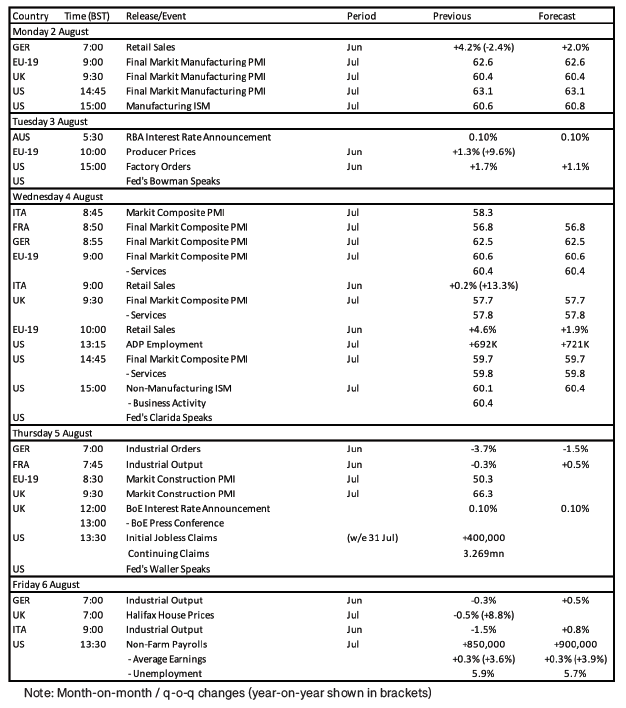

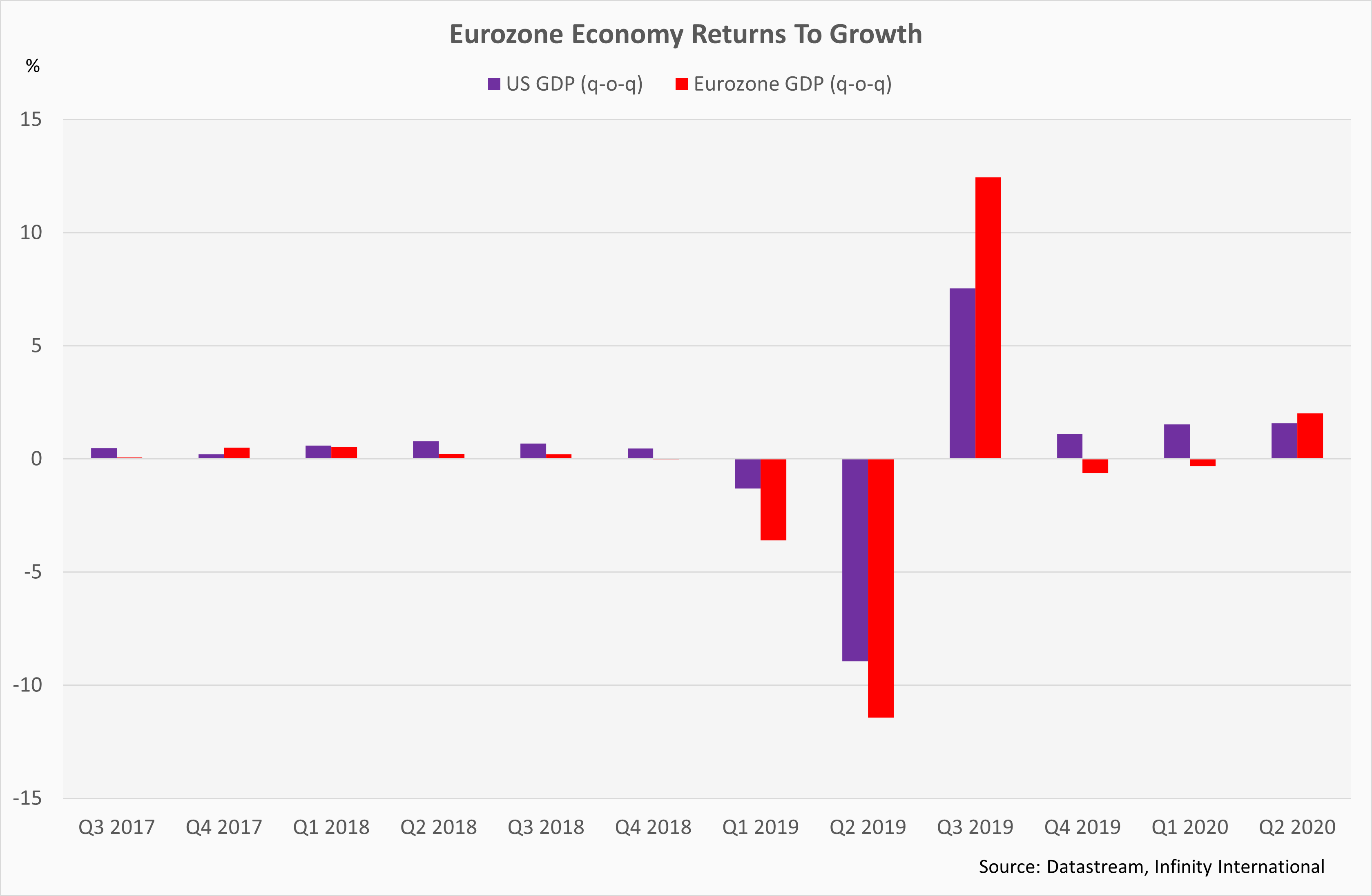

Last week brought the release of much anticipated Q2 GDP figures from the eurozone and the US. Economic projections at present reflect more than a little guesswork, given the uniqueness of the crisis and subsequent rebound, so the data provided the first real insight into whether the impressive growth rates pencilled in by analysts are realistically attainable.

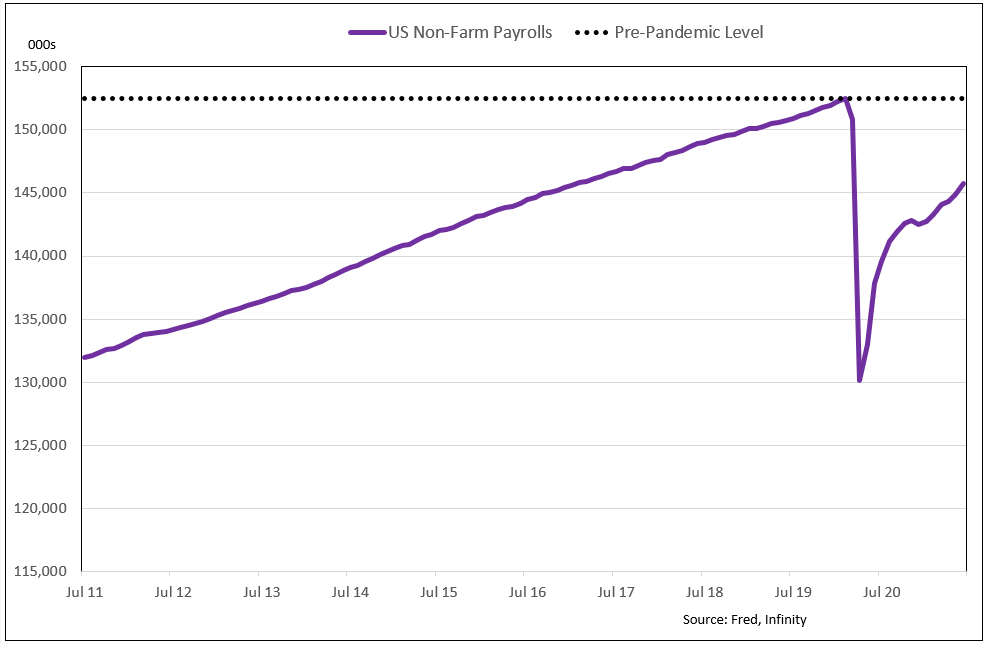

In the case of the US, the Q2 data suggested that lofty projections for growth (2021 consensus forecast: 6.6%) may be overly optimistic. The economy grew by a solid 1.6% q-o-q and returned to its pre-pandemic level, but this was well below expectations for a 2.1% rise. It is not quite time to sound the panic alarm, however, with the underlying breakdown showing that the slowdown was at least in part a function of supply chain disruptions that will fade. Firms ran down inventories sharply for a second straight quarter, which has subtracted around 1.0 percentage point from growth but represents money in the bank for H221 and H122. High capacity utilisation rates, robust growth in durable goods orders (+3.0 q-o-q in Q2) and strong consumer spending (+ 2.8% in Q2), indicates that softness in business investment is also due to supply chain issues and can be expected to recover in the coming quarters.

In contrast, the Q2 data suggested that analysts may be underestimating the recovery in the eurozone (2021 consensus f’cast: 4.5%). Output expanded by an impressive 2.0% q-o-q (f’cast 1.5%), with particularly strong growth rates observed in periphery economies such as Spain (+2.8%) and Italy (+2.7%). This more than compensated for weakness in Germany (+1.5% q-o-q vs f’cast +2.0%), where activity was held back by supply chain issues that are creating major headaches for the crucial auto sector. An underlying breakdown is not available at a eurozone level, but national figures suggest that activity was unsurprisingly driven by a release of pent-up demand associated with the easing of lockdowns and another solid performance for the key export sector.

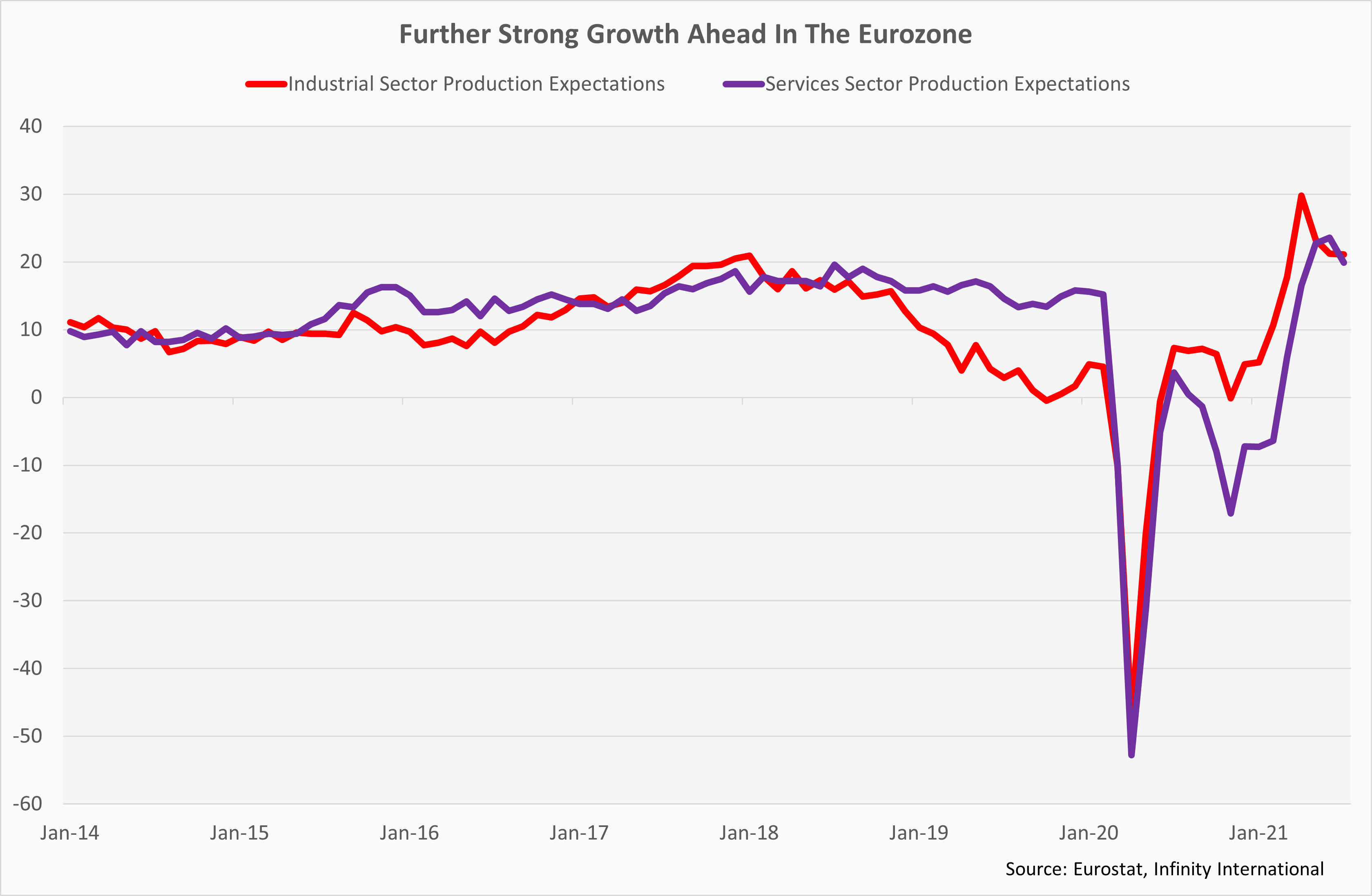

Indications are that eurozone growth will remain impressive in the coming months, reflecting the fact that the continent’s sluggish vaccine rollout means that it is at an earlier stage of the recovery. Lockdowns were only rolled back in May, after a third wave of infections hit the continent in April. This suggests there is scope for further strong growth in consumer spending, with an ongoing improvement in labour market conditions acting as a further tailwind. The unemployment rate dropped to 7.7% in June, though it remains flattered by the impact of furloughing programmes. The European Commission’s (EC) sentiment index also hit a record high in July, while business capacity utilisation rates are holding well above historical averages (82.9% versus 82.0%).

Overall, the data have not significantly altered our view on the outlook for the dollar, with incoming strong macro data and a hawkish Fed likely to see the greenback remain supported in the near-term. We did see some dollar weakness emerge last week, but in our view this mostly reflected a combination of profit-taking and month-end flows.

In terms of the euro, we are gradually growing less downbeat on its near-term outlook. Previously, we have guided that monthly indicators would begin to point to a slowdown in activity in the eurozone from end Q321, led by softness in manufacturing, and this would see the single market currency soften. As of July, though, the demand picture remains very strong, notwithstanding the threat posed by the spread of the delta variant, with the forward-looking components of the EC’s sentiment indices remaining consistent with strong growth. Combined with above-target inflation (2.2% y-o-y in June) that will create something of a communications challenge for the ECB in the coming months despite its attempt to push a dovish line, we expect that relative euro strength could persist for some time yet, reducing the scope for GBP/EUR to push above year-to-date highs near €1.18 before end Q321.

Dollar

The highlight of the US schedule is the release of the July employment report on Friday. Non-farm payrolls are forecast to have increased by 900k after an 850k rise in June (strongest gain since last August), driven by re-opening effects and the move by several Republican states to discontinue benefit top-ups. However, risks to the forecast are tilted to the downside, given the persistence of the pandemic. Survey data from Indeed suggest that fear of the virus is a significant factor explaining softer than anticipated labour supply growth despite strong demand for workers. Cynics have suggested that it is the availability of enhanced jobless benefits that has resulted in workers remaining on the side-line, so this week’s data look set to offer some clarity on what the dominant factor behind depressed labour supply is really.

In terms of the other key points from the employment report, the jobless rate is projected to have dipped to 5.7%, after unexpectedly ticking up to 5.9% in June after the prime age labour force participation rate rose. Meanwhile, the ongoing imbalance between labour demand and supply is anticipated to have seen average earnings increased by 0.3% m-o-m in July (3.9% y-o-y). Overall, an extremely wide forecast range for the key payrolls figure (400-1,600k), a reflection of the diverse factors impacting the data, suggests that we will need a significant surprise to generate any major reaction in the dollar, with risks clearly two-sided. Earlier in the week, we will get the ISM surveys for July, which are likely to point to a modest easing of growth as catch-up effects continue to fade and supply chain issues persist.

Sterling

The Bank of England’s August policy meeting is the main draw in the UK this week. Two officials recently called for the central bank to prematurely end its asset purchase programme in the coming months, arguing that with inflation running at 2.5% y-o-y in June (target: 2.0%), it is difficult to argue that the economy requires further policy support. Indications are that the hawks remain in the minority, meaning policy changes do not appear to be on the cards. However, the voter breakdown will be of significant interest (June: 8-1, with the dissenter Andy Haldane since leaving the bank). Should more than two officials vote for the removal of policy supports, we could see sterling attract decent support.

Traders will also look to the central bank’s Q3 Monetary Policy Report, which will contain updated macro projections, for clues on the trajectory for policy. In May, the BoE implicitly endorsed market pricing for a 15 basis point (0.15%) rise in the Bank Rate to 0.25% by Q322 as it forecasted that inflation would hold near 2.0% in Q422 even in the event of such a hike. Key here will be the central bank’s updated view on the outlook for the unemployment rate following the end of furlough in September. Under its latest forecast, the BoE forecasts unemployment at 5.8% by end Q4 (currently 4.8%), though we have since seen that the end of similar programmes in the Antipodeans did not result in a rise in unemployment.

In the more immediate future, we will see a significant upward revision to the central bank’s 2021 inflation projection, as incoming data are coming in significantly hotter than envisaged on the back of major demand-supply imbalances. However, this will have limited implications for monetary policy, with Governor Bailey continuing to guide that inflation will subside as demand-supply imbalances are corrected. More generally, it will be interesting to see how the central bank accounts for the ‘pingdemic’ in its GDP forecasts, given the central bank’s forecast for 7.3% growth in 2021 is near the top of the forecast range (Reuters: 6.7%).

Euro

The eurozone macro schedule includes retail sales and German industrial production figures for June, though euro impact will be limited as GDP data for Q2 are already available (+2.0% q-o-q). A 1.9% m-o-m increase is pencilled in for retail sales after a 4.6% rise in June, with the slowdown reflecting the fading boost from re-opening effects and a switch from goods to services expenditure. Meanwhile, German industrial output is projected to have risen by 0.5% m-o-m after unexpectedly dropping by 0.3% in May, with activity in the key auto sector ticking up slightly in June as supply chain issues eased.