Production backlogs and transportation bottlenecks (quite literally in the case of the Suez Canal blockage) have emerged as a major headache for businesses this year as recovery from the pandemic has continued to throw up additional headwinds. These disruptions held back growth across western economies in Q2, with industrial activity particularly badly impacted as the sector struggled with significant shortages of inputs. The situation in the UK has been exacerbated by the impact of Brexit, with goods trade volumes with the EU down some 23.1% on 2018 levels in Q121 relative to a 0.8% decline in trade with the rest of the world as UK-based importers and exporters have had to cope with the new trading rules and additional paperwork associated with leaving the customs union.

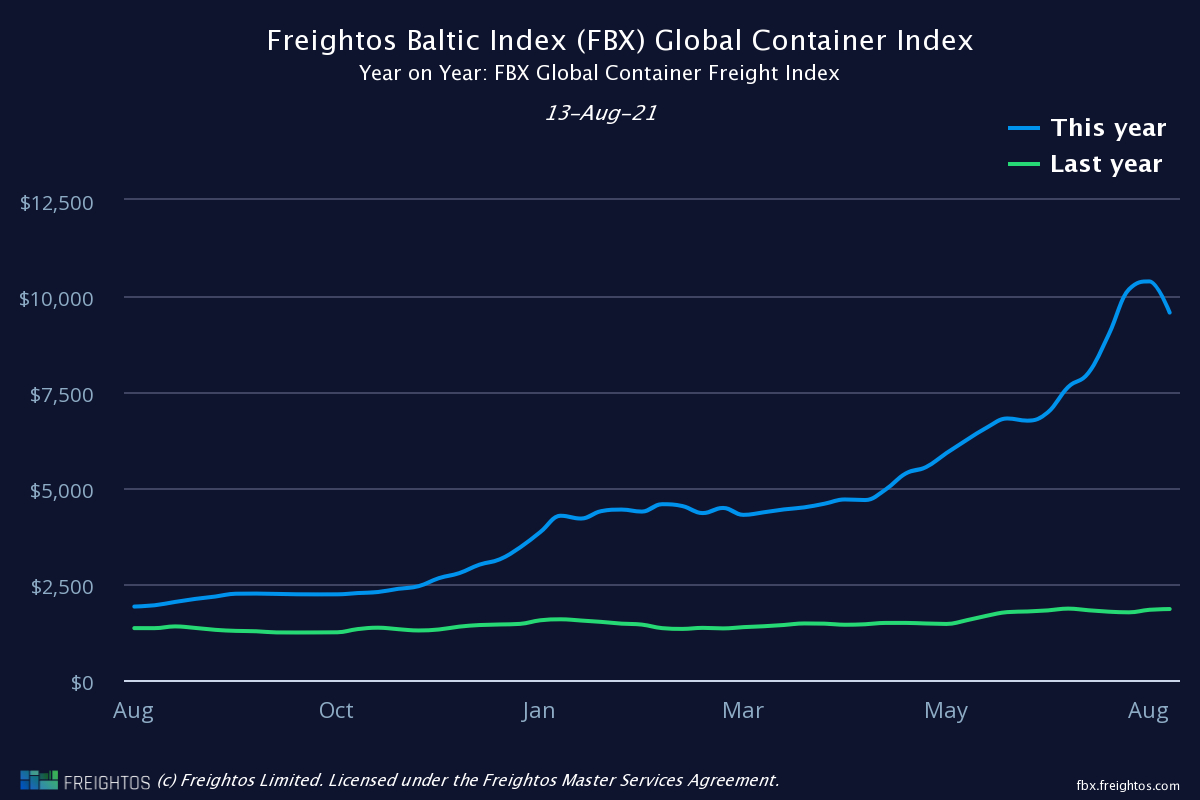

In addition to holding back growth, supply chain issues are also a key factor behind the increase in price pressures we are observing everywhere. Producer price inflation rose to a decade high in the US and Germany last month, with a 418% y-o-y jump in freight costs per the Freightos Baltic Index a significant contributing factor. Granted, PPI doesn’t feed perfectly across into the consumer price index, but given elevated demand as households splurge post lockdown there is certainly increased scope for businesses to protect their margins and pass these costs onto consumers.

Central to the emergence of these disruptions has been the lagging recovery in supply relative to that of demand, with the former having benefited from the availability of significant government income supports that meant goods expenditure held up reasonably well over the course of the pandemic. In contrast, a diverse range of factors has hampered the rebound in supply, including:

- Businesses underestimated how swift the recovery in goods spending would be and failed to plan accordingly. For instance, freight companies took capacity offline on the assumption that the rebound in international trade flows would prove prolonged, as in the aftermath of the 08/09 crisis. This created second-order effects as shipping containers were also left stranded.

- The persistence of the pandemic, resulting in work stoppages on the back of self-isolation requirements. While these pressures are easing in western economies thanks to efficient vaccine rollouts, we are seeing a sharp slowdown in manufacturing activity in the ‘world’s factory of Southeast Asia as it struggles to contain the Delta variant.

- On a related note, self-isolation requirements are also significantly disrupting transportation networks, with China partially closing the world’s 3rd busiest port at Ningbo-Zhoushan on August 11 in response to a local outbreak. Previously, the closure of the Yantian port in late June was estimated to have had as significant of an impact on global trade as the Suez Canal blockage.

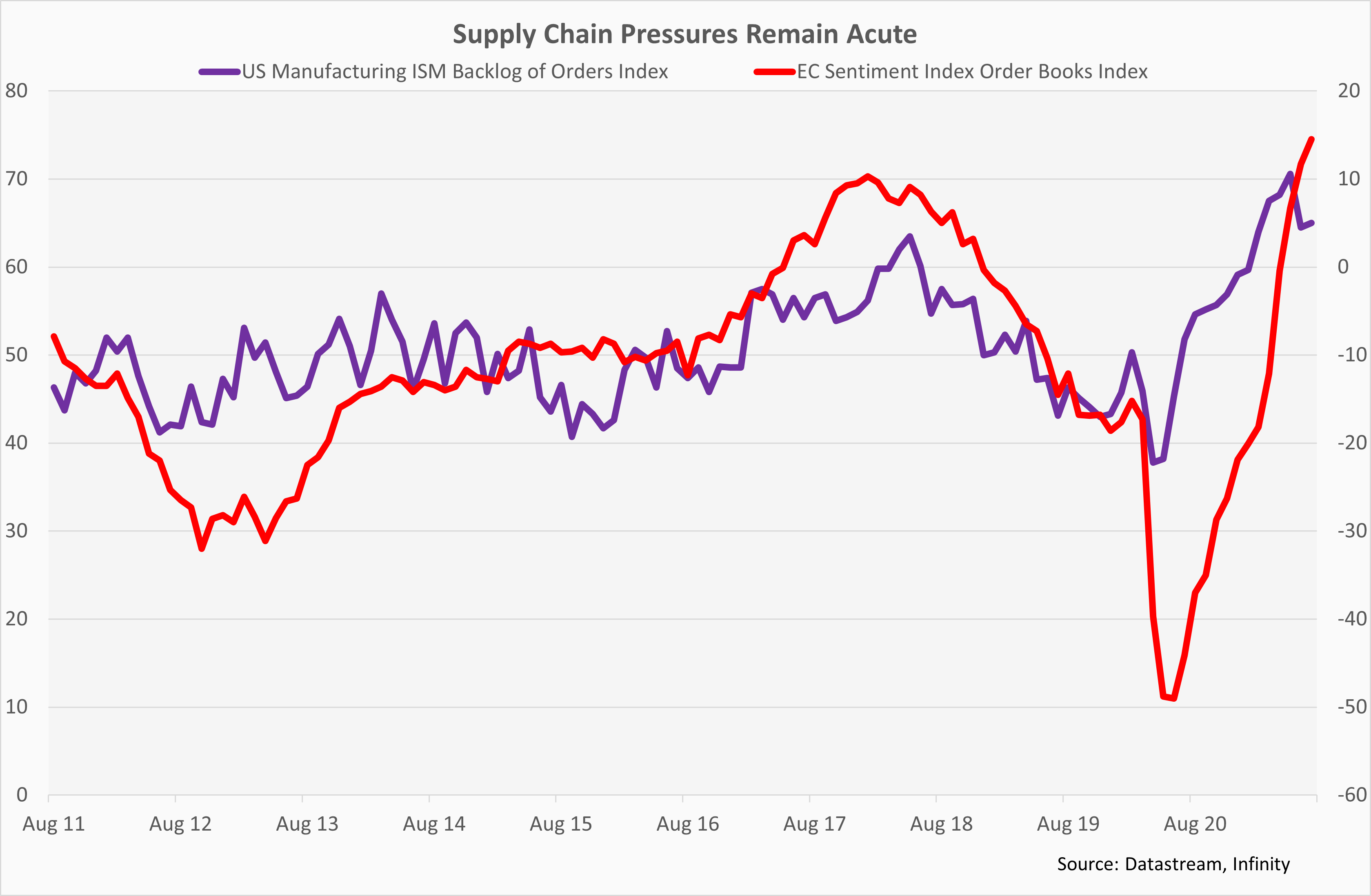

Orders backlogs hit another record high in the eurozone and US in July, with activity in the former’s key auto sector struggling with a major shortage of semiconductors that have left activity some 34% below pre-pandemic levels in Germany. On the positive side, freight costs are showing some signs of peaking, but rates remain well above norms and industry experts are guiding that it will be mid-2022 until imbalances in relation to where shipping containers are located are corrected. This timeline could be pushed back further should the pandemic continue to disrupt global trade, particularly given China has yet to abandon its zero-Covid strategy amid question marks over the effectiveness of domestically produced vaccines.

Supply chain disruptions should eventually be resolved as demand-supply imbalances are gradually lessened and vaccines more widely rolled out across the developing world. However, the timeline remains hazy, with a normalisation of conditions before end-year appearing unlikely. The shift from goods to services expenditure underway in western economies that have re-opened will help matters on this front, but this will take some time to feed across into a meaningful reduction in orders backlogs given firms will also have to replenish inventories that have been sharply run down. Similarly, while we expect that firms will invest in an additional capacity that will allow them to meet demand, the impact of supply chain issues themselves are prolonging this process. Overall then, it is hard to avoid the conclusion that a return to normality will be delayed until at least 2022.

Dollar

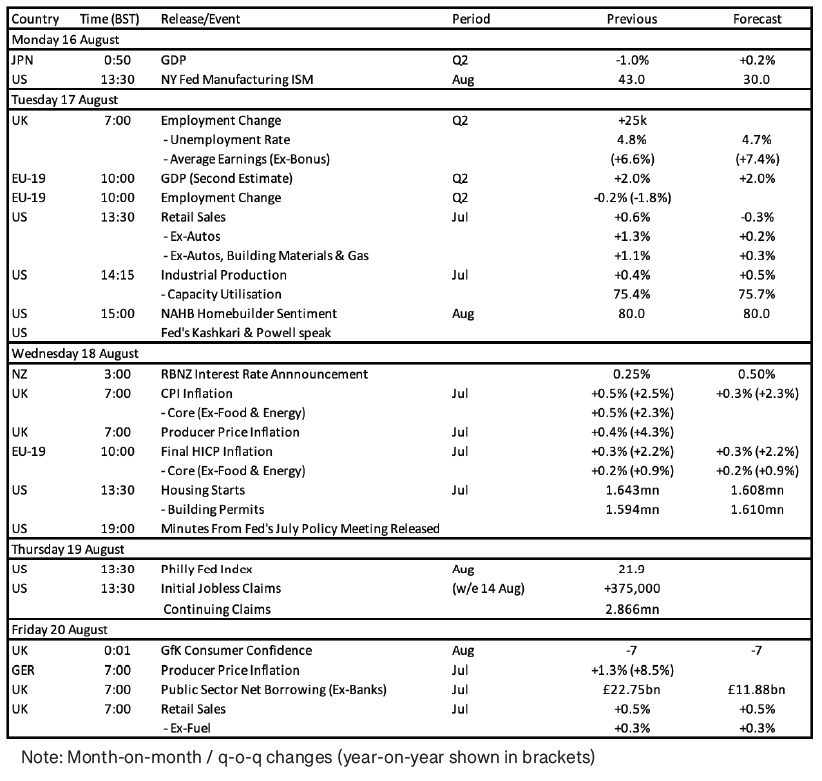

This week will bring a couple of updates from the Fed, with Chair Powell scheduled to speak on Tuesday and the minutes from the central bank’s July policy meeting set for release on Wednesday. Powell’s comments will attract the lion’s share of attention, as traders look for any insight into whether incoming strong US macro data (and in particular robust labour market figures) have prompted a shift in his view on the appropriate timeline for the central bank to begin tapering its asset purchase programme. They may, however, be left disappointed as Powell has previously indicated that he wanted to see several months of +850k payroll prints (+943k in July) before contemplating removing policy supports. Signs that price pressures are beginning to moderate, after core CPI inflation eased to 4.3% y-o-y in July from 4.5% in June, and disappointing consumer sentiment data also offer scope for Powell to remain in wait-and-see mode. In any case, we believe that Powell is unlikely to signal any major policy shift before his keynote speech at Jackson Hole.

On the data front, July retail sales and industrial production figures will be of some interest. With respect to the former, we see scope for retail sales to dip by more than the projected 0.3% m-o-m, given the earlier date of Amazon Prime Day likely resulted in households front-loading expenditure in June. A weak retail sales print will not be a cause for too much alarm, however, given the focus has shifted on to what extent that services expenditure is rebounding now that Covid restrictions have been largely rolled back. In terms of industrial production, the consensus projection is for a 0.5% m-o-m, though forecasting manufacturing activity is a bit of a guessing game at the moment due to the prevalence of supply chain shortages.

Sterling

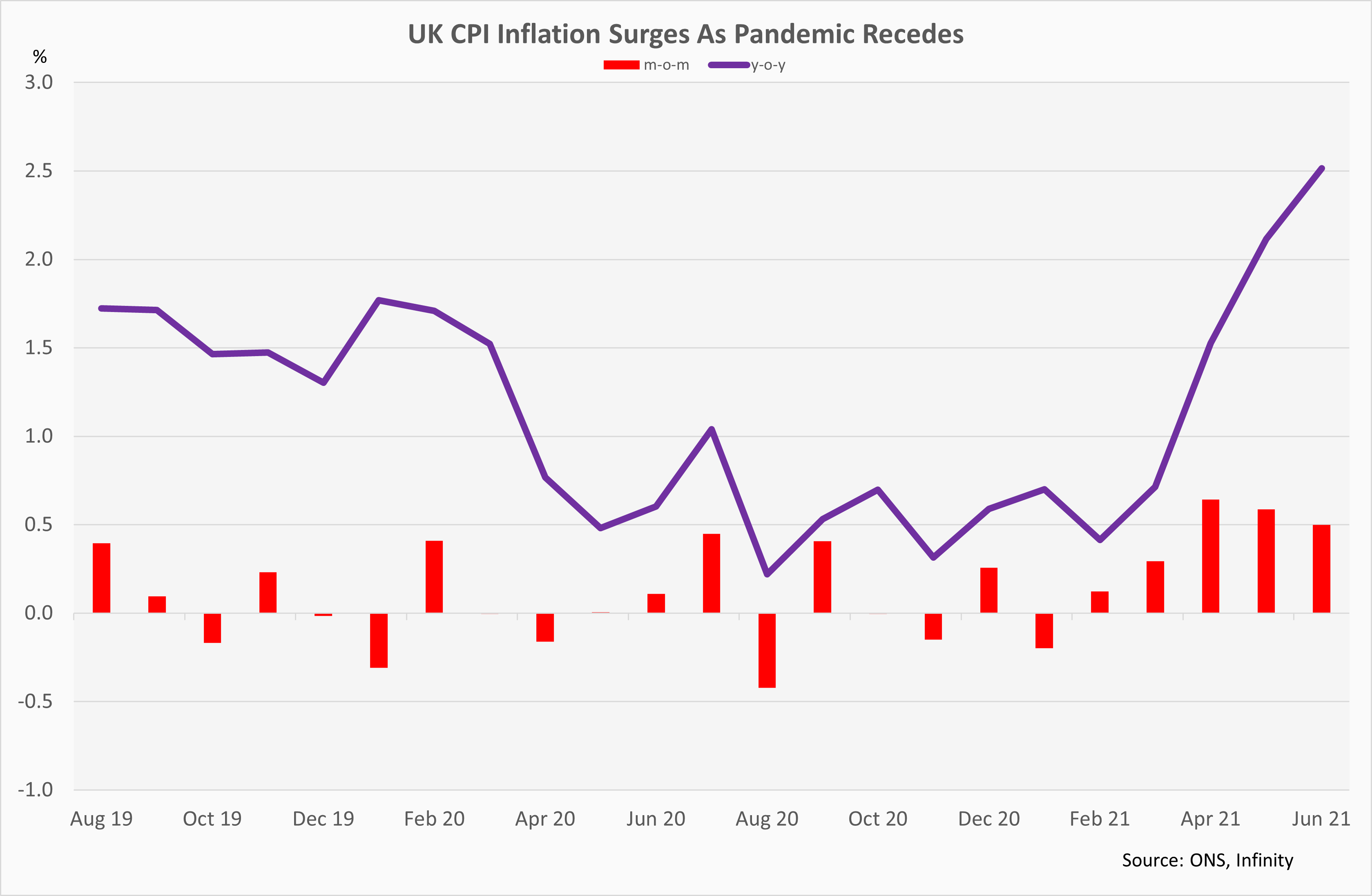

A busy calendar lies ahead in the UK, with CPI figures for July the highlight. Leading indicators suggest that price pressures remained acute in the month, with the input cost subcomponent of the UK’s service sector PMI rising to a record 25-year high on the back of worker shortages (linked to reduced immigration and the pingdemic) and supply chain issues. The evidence suggests that strong demand as households continue to splurge post lockdown allowed firms to pass these increased costs onto consumers, with the prices charged sub-component of the services PMI also hitting a record high in the month. Overall, analysts forecast that the CPI index rose by 0.3% m-o-m as a result, though this would see the y-o-y inflation rate slow to 2.3% on the back of adverse base effects linked to last year’s re-opening. Significant risks surround the outlook, with the timing of sales knocked out of kilter by the impact of the pandemic.

The other main highlight in the UK this week will be the release of Q2 employment data, with consensus forecasting that the unemployment rate dipped down to 4.7%. The focus, however, will be on the timelier components of the report, in particular the updated payroll and job vacancy figures for July. We expect that the data will point to a further tightening of labour market conditions as the impact from ‘Freedom Day’ that saw the remaining restrictions on economic activity removed feeds through. Looking ahead, the expiration of the Job Retention Scheme looms at end-September, with 1.9mn workers remaining on furlough per the latest official figures dated end-June. However, timelier estimates from the ONS suggest that this number dropped back down to circa 1mn in early August. Overall, the BoE anticipates that its ultimate end-date will have minimal impact on the headline unemployment rate, which it anticipates will rise to just 5.2% in Q422 given evidence of strong labour demand.

Euro

A quiet week lies ahead in the eurozone, with no notable release on the schedule. Second estimates of eurozone Q2 GDP and July inflation are due, but significant revisions to the data are not anticipated.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).