Dollar

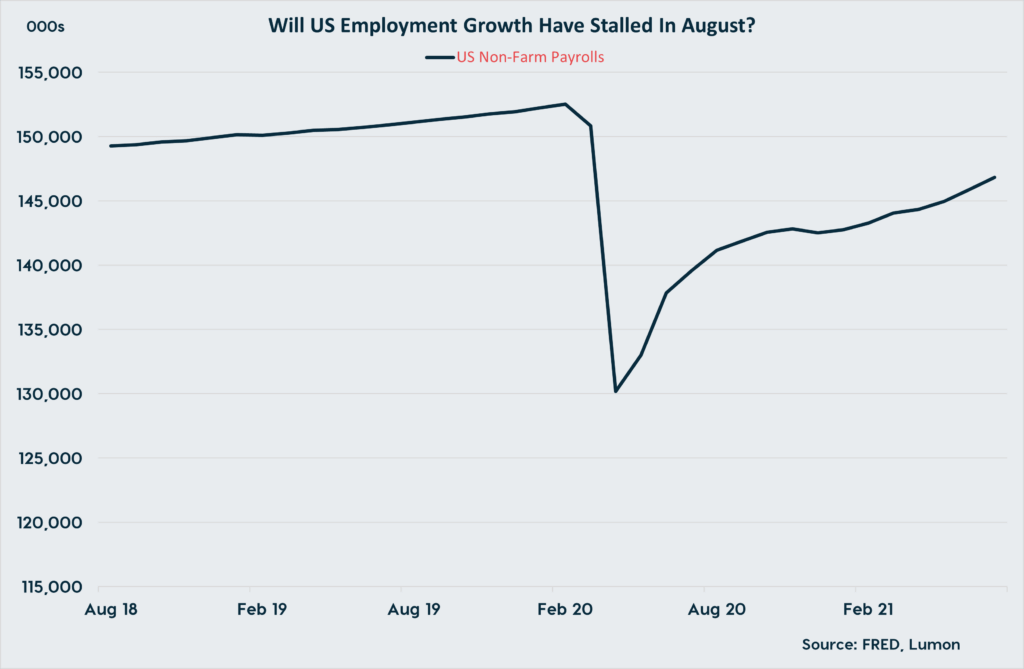

The dollar came under some further modest pressure yesterday, with GBP/USD breaking through resistance at $1.38 and trading up to the $1.383 mark. Meanwhile, EUR/USD continued to trend higher and pushed into the upper half of the $1.18-1.19 range. There was no single catalyst for the move, which we suspect was due to markets repositioning ahead of the much anticipated US employment report for August that is due today.

The data have loomed large in the minds of traders since the release of the July Fed meeting minutes, when the central bank sent a strong signal that it would be inclined to taper its asset purchases (currently buying $120bn of bonds a month) if labour market growth holds up over Q3. Since then, payrolls increased by an impressive 950k in July, with expectations growing that if we see a similarly strong report today then a tapering announcement could come as soon as the September FOMC meeting. Importantly, while Fed Chair Powell adopted a dovish tone during his key note speech at Jackson Hole last week, he did not push back heavily against this narrative.

Indications are that we are unlikely to see a sufficiently strong report today, reflecting a surge in Covid-19 cases linked to the spread of the delta variant. US economic data have generally printed on the soft side in recent weeks, with August PMIs and consumer confidence figures pointing to a significant slowdown in growth in the month. Consensus anticipates that today’s employment report is unlikely to buck this trend. The closely watched non-farm payroll figure is expected to come in at roughly +750k, though Bloomberg’s ‘whisper’ number suggests that true consensus now lies below 700k after some further disappointing data releases this week.

As a result, it may be the case that we will require a major downside miss today to generate a significant reaction in the dollar and if anything risks are tilted to the upside. While the release appears likely to prompt some FX market volatility, we are sceptical that it will significantly change the course of Fed policy. Ultimately, it is clear that tapering is coming in the next 6 months and the big question is when interest rate hikes will follow. We expect the tightening cycle will commence in Q422, but it will take more than one jobs report for this timeline to become apparent. In the interim, it is unlikely dollar strength will be significantly unwound, with inflation holding well above target, weak labour supply rather than demand the most likely explanation for any soft jobs reports and the Fed remaining divided on the appropriate trajectory for policy.

Euro

There is little out to influence the euro today, with the action in the single market current set to be largely driven by the reaction in FX markets to the non-farm payrolls number in the US. Yesterday, producer producer inflation for August came in on the hot side again (12.1% y-o-y vs fcast 11.0%) on the back of higher energy costs. An uptick in eurozone price pressures will dominate the discourse over what is left of H221, with surging gas prices set to drive inflation higher.

Sterling

There is a quiet look to the macro schedule to end the week in the UK. Some of the shine has come off sterling since early August, by incoming strong inflation data and the hawkishness of the BoE will act as tailwinds in the coming weeks.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).