Dollar

The action on currency markets yesterday was confined to relatively narrow trading ranges, with the dollar remaining reasonably well supported. This was reflected in GBP/USD trading in the lower half of the $1.38-1.39 range, while EUR/USD at times tested below the $1.18 threshold. There has been little out to provide direction over the past 24 hours, with the macro schedule devoid of any possible market-moving releases. At the same time, investor sentiment has remained fragile as traders continue to question whether we are on the cusp of a relatively sizeable pullback in equity markets.

Today, the focus will be on the release of CPI figures for August, which will pose two-sided risks to the dollar. The data are forecast to point to a modest easing in the year-on-year rate of inflation from 5.4% to 5.3%. This will be driven by an easing of price growth in sectors most sensitive to the re-opening of the economy (i.e. hospitality and transport), as well as a drop in used car prices (a spike in prices contributed to a significant increase in inflation in May/June). Price pressures are projected to have broadened in August, reflecting a combination of major supply-side issues (transportation bottlenecks and labour shortages) and a surge in pent-up demand post lockdown, which will partly undermine the Federal Reserve’s view that elevated inflation will prove transitory. Indeed, whereas in Q1 inflation was expected to ease below its 2% target by end-year, it is now likely to hold above 3%.

Owing to the persistence of these elevated price pressures, which are beginning to push inflation expectations higher also, we anticipate that the Federal Reserve will turn increasingly hawkish in the coming quarters. This in turn should provide a solid backdrop for the dollar and help to counteract seasonal greenback weakness.

Sterling

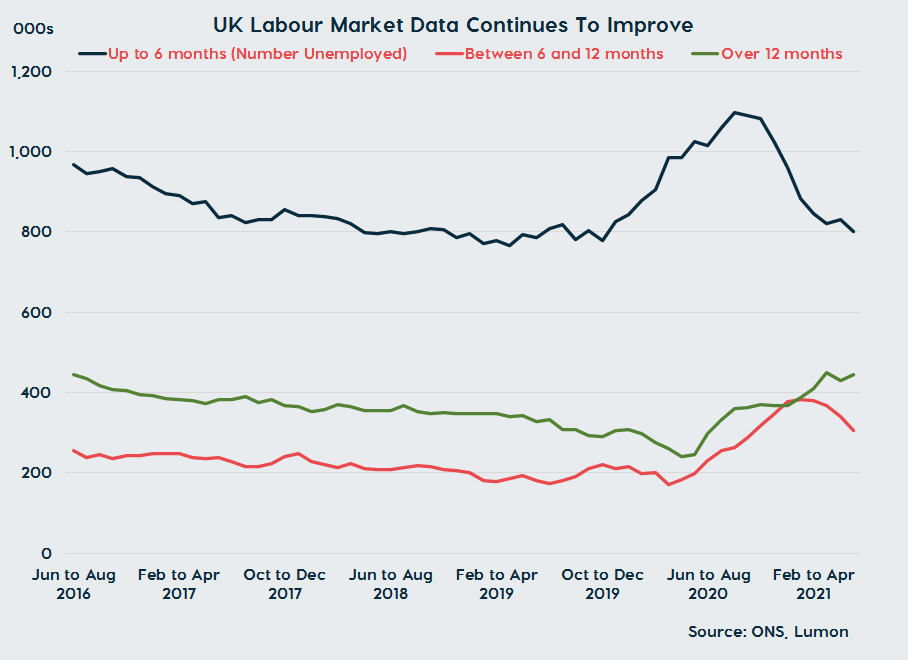

In the UK, sterling was minimally impacted this morning by the release of July/August jobs figures, with GBP/EUR holding above €1.17. Overall, the data did point to a continued improvement in labour market conditions, though the Job Retention Scheme (due to expire at end-September) is clouding the picture somewhat. The unemployment rate held at 4.6% in the three months to July, while there was still no sign of a pick-up in redundancies ahead of the end of furlough, and job vacancies have hit another record high. PAYE payrolls returned to pre-pandemic levels in August, while underlying wage pressures remained strong amid ongoing shortages of workers.

As we’ve previously highlighted, the Bank of England views these shortages as structural (a result of Brexit and the pandemic prompted early retirements) and is growing increasingly concerned that wage inflation may prove persistent. The central bank appears to be leaning toward beginning its interest rate hiking cycle in 2022, in line with our view, in a development that we anticipate will see sterling push higher again on a 12-month horizon. In terms of the rest of the day, however, there is little out to impact sterling, with the focus from a fundamental perspective shifting to the release of August CPI inflation figures tomorrow morning.

Euro

Over in the eurozone, the schedule remains quiet, with little data out this week. The German election (due to be held on 26 September) does remain of interest, with polling data suggesting that the centre-left Social Democratic Party will unseat the centre-right Christian Democratic Union, which has held power since 2005. However, the contest has not yet really emerged as a driver of the euro.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).