Dollar

The dollar came under some very marginal pressure yesterday as investor sentiment continued to improve. GBP/USD drifted back up toward the midpoint of the $1.37-1.38 band and EUR/USD pushed above resistance at the $1.175 mark. Data-wise, there was little out to influence the currency, with the release of durable goods orders for July (a leading indicator for business investment) going largely unnoticed. The data came in broadly in-line with expectations, with a 0.1% m-o-m dip in the headline index a function of lower aircraft orders that had been anticipated. The core index (ex-aircraft and defense) was flat, however, suggesting that business investment may have lost some momentum at the beginning of Q3, though orders remain well above pre-pandemic levels.

Looking to the day ahead, there isn’t too much out to excite markets, with weekly jobless claims figures for the week ending August 21 the highlight. Despite the quiet schedule, we see scope for the dollar to remain on the back foot over the next 24 hours given the still favourable risk backdrop. However, we may struggle to touch the highs in GBP/USD near $1.395 seen in early August as the greenback is likely to remain reasonably well supported ahead of Fed Chair Powell’s speech at Jackson Hole on Friday afternoon.

Euro

The euro continued to move higher yesterday, despite the German Ifo (a closely watched measure of business sentiment) dropping to a three-month low in August. The fall reflected expectations of weaker future growth and was broad-based, with the data pointing to softening activity in the manufacturing and services sectors. This reflected a combination of supply chain issues, weak export demand (due to the slowdown in China) and the spread of the delta variant. FX markets, however, were unphased and GBP/EUR held within its range in the upper half of €1.16-1.17.

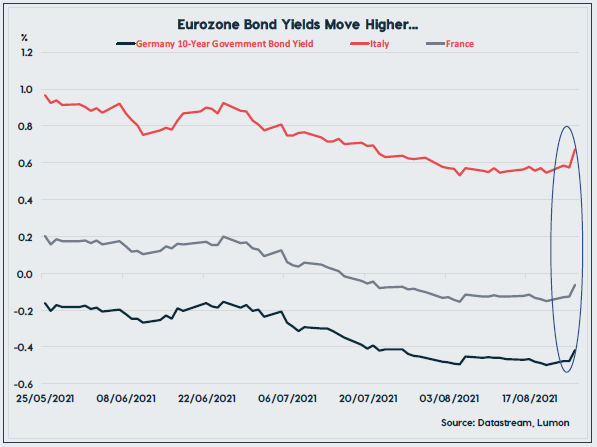

Looking to the day ahead, as in the US the schedule is devoid of any market-moving releases. However, the release of the ECB’s account of its July policy meeting ahead of the next meeting this day two weeks. To our surprise, eurozone bond yields have begun to creep up in recent days, with German 10-year yields at their highest level in a month as some ECB policymakers have emphasised the emergency nature of the central bank’s Pandemic Emergency Purchase Programme, hinting that bond buying activity may be scaled back in the coming quarters. Despite the moves, our base case remains that policy normalisation is some distance away, as underlying inflationary dynamics remain weak due to persistently high unemployment.

Sterling

Over in the UK, the calendar will again offer little direction to sterling today. However, the latest set of real-time indicators from the ONS will be of some interest, as we wait to see whether signs of a pick-up in economic activity relative to July persist. We will also get an updated estimated estimate of the number of workers on furlough in early August. The PMIs suggested that employment growth remained robust in the month, indicating that the numbers on the Job Retention Scheme may have fallen below 1mn ahead of its expiration next month.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).