Dollar

The dollar remained on the front foot yesterday, with GBP/USD drifting down below the $1.38 threshold and EUR/USD pushing down toward the midpoint of the $1.18-$1.19 range. The action coincided with a minor sell off in both equities, with the main European indices shedding around 0.5% and the S&P 500 dipping by 0.3%, and bond markets where German and US 10-year yields rose by 5bps (inverse relationship between yields and price). The main asset classes are increasingly correlated, which could amplify the negative impact from any pronounced sell-off.

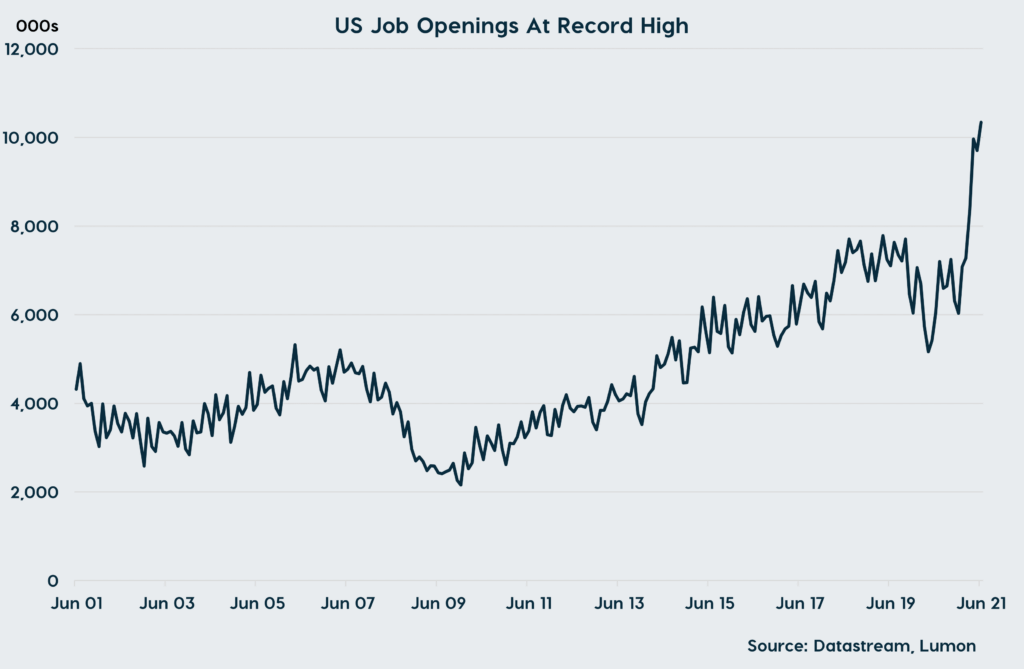

Data-wise, there isn’t much out to offer direction today, with July’s Job Opening and Labour Turnover figures unlikely to be a market mover. Consensus anticipates that vacancies rose to a fresh high in the month, though the figures are outdated by this point. There are concerns that a delta variant-driven surge in COVID-19 cases may have weighed on labour demand in August after non-farm payrolls rode by just 235k (f’cast 750k) in the month. However, this is difficult to square with survey indicators (ISMS and NFIB jobs report) suggesting firms struggled to fill positions in the month, which appeared to prompt a robust 0.6% m-o-m rise in average hourly earnings. It will be interesting to hear what Fed officials think about the prospect of a wage-inflation spiral emerging, with several officials due to speak today.

Sterling

The modest bout of risk aversion coincided with some sterling weakness yesterday, with GBP/EUR drifting back into the lower half of the €1.16-1.17 band. The currency found no support from a relatively upbeat set of comments from Bank of England official Michael Saunders, the most hawkish member of the Monetary Policy Committee, who indicated that he saw some scope for the interest rate hiking cycle to begin next year if growth remains strong and inflation holds persistently above its 2% target, as the central bank is currently forecasting will be the case. Importantly, despite the drag from the ‘pingdemic’ and supply chain issues, Saunders believes GDP may have already returned to pre-pandemic levels, a remarkably fast recovery made possible by the government’s fiscal stimulus measures.

The fiscal backdrop, however, will emerge as a headwind to growth, and in turn sterling, in the coming quarters as the Conservative party adopts an increasingly hawkish tone. Yesterday, it was confirmed that National Insurance rates will be raised by 1.25 percentage points from April 2022, with the additional monies set to be initially used to help clear the NHS backlog before being used to fund social care reforms. This comes on top of Chancellor Rishi Sunak’s previous announcement as part of the March budget that income tax thresholds will be frozen until 2026, an effective tax hike given wages typically rise by 3% an aggregate per annum. The rise in taxes can at least partly be attributed to the impact from a permanent reduction in the size of the potential labour force (and hence tax base) following the introduction of new restrictions on migration post-Brexit.

Euro

Over in the eurozone, the single market currency has remained reasonably well-supported in the lead-up to tomorrow’s European Central Bank meeting. As we highlighted on Monday, we believe that those expecting a hawkish outcome to the meeting are likely to be disappointed and we remain of the view that GBP/EUR could push back up toward €1.17 on Thursday afternoon, absent a notable deterioration in risk appetite between now and then.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).