Sterling

Sterling at times came under pressure yesterday as investors remained in risk-off mode, which saw GBP/USD and GBP/EUR trade to intra-day lows near $1.373 and €1.161 respectively. The currency subsequently found support from a series of hawkish comments from several Bank of England officials in the afternoon, with GBP/USD rising back into the $1.37-1.38 band and GBP/EUR pushing to the €1.165 mark.

The central bankers indicated that they continued to characterise the strong inflation they expect to see over H221 (peaking at 4% in December 2021) as transitory. However, there is a risk that persistent labour shortage could result in wage growth remaining elevated for some time and this could create upside risk for inflation. Officials anticipate the conclusion of furlough at the end of this month will see recruitment difficulties ease somewhat, but a more critical issue is that the size of the overall labour force may have shrunk due to Brexit and a drop in labour force participation (increase in numbers attending university / retiring early) as we have previously flagged. Today, there is little out to influence sterling, but with markets remaining in risk-off mode we expect GBP/USD to trend lower.

Euro

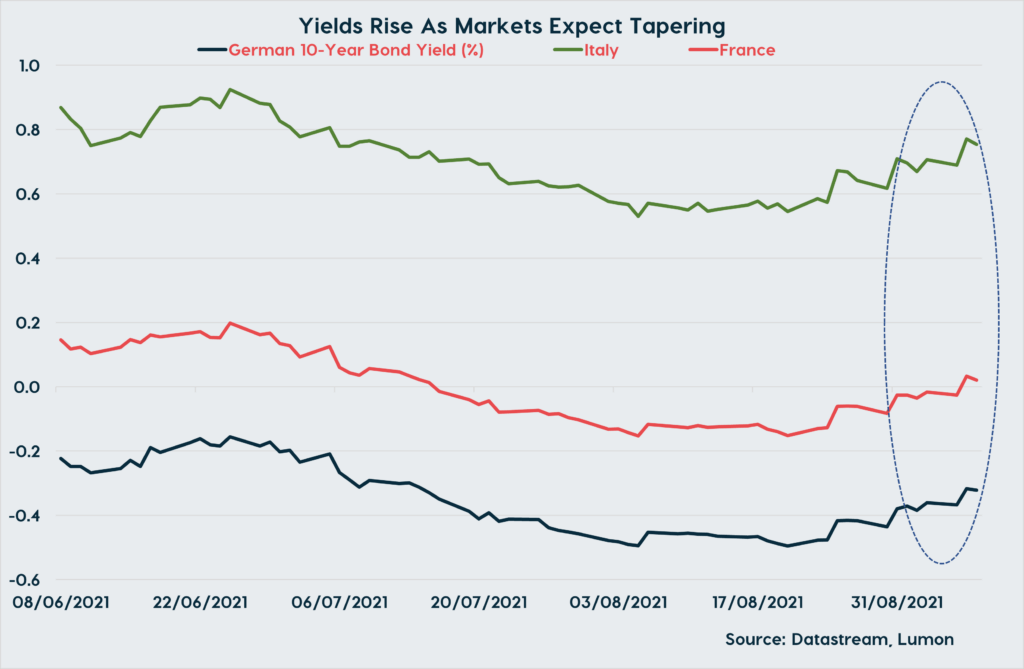

Meanwhile, EUR/USD trended back down toward the $1.18 threshold ahead of the today’s ECB policy meeting, though this was more of a function of dollar strength linked to the latest bout of risk aversion. We see scope for the single market currency to come under some further downward pressure today, given our expectation that the ECB may disappoint those anticipating that it will announce a modest reduction in the pace of its monthly asset purchases. Granted, eurozone growth came in stronger than envisaged in Q2 and the economy may achieve its pre-pandemic level in Q3, while headline inflation will remain well above its 2% target through H221. However, indicators suggesting activity is already easing rapidly, while elevated price pressures are largely a function of base effects and transitory factors stemming from supply chain issues.

More importantly, we believe that a move by the central bank to begin tapering would be inconsistent with its only recently announced commitment to adopt especially forceful easing measures when interest rates are at their lower bound, which President Lagarde has confirmed they are now. What is more, being seen to act before the Fed, who are likely to delay tapering until Q4, would be difficult to square with the central bank’s attempt to ‘out-dove’ peers in the year-to-date.

If we are incorrect and the central bank does taper, we expect that the upside for the euro will be partly capped by the fact that the move is likely to be framed in dovish terms, with Lagarde possibly guiding that asset purchases will remain elevated through 2022. Chief Economist Philip Lane has previously eluded to the fact that central bank’s traditional Asset Purchase Programme could be beefed up to loosely match eurozone bond issuance next year to reduce the impact from the expiration of the Pandemic Emergence Purchase Programme (currently the main asset purchase programme).

Dollar

Elsewhere, there is nothing out to offer much influence the dollar today, which we expect will remain reasonably well-supported as investor sentiment remains mixed. Yesterday, the Fed’s Beige Book (qualitative assessment of economic conditions) suggested that supply chain issues remain extreme and firms are continuing to struggle to attract workers, another release suggesting above-target inflation will persist for some time.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).