Dollar

The dollar retraced some of its losses that followed the release of a mixed August employment report yesterday, though volumes were light as the US was shut for a market holiday. This saw GBP/USD drop back into the lower half of the $1.38-1 39 band, while EUR/USD pushed back away from the $1.19 threshold. The modest gains for the greenback came despite a solid improvement in investor risk appetite, with the main European and UK equities up 0.50-1.00%. Today, there is little out to provide direction from a data perspective in the US, suggesting any moves will be sentiment driven.

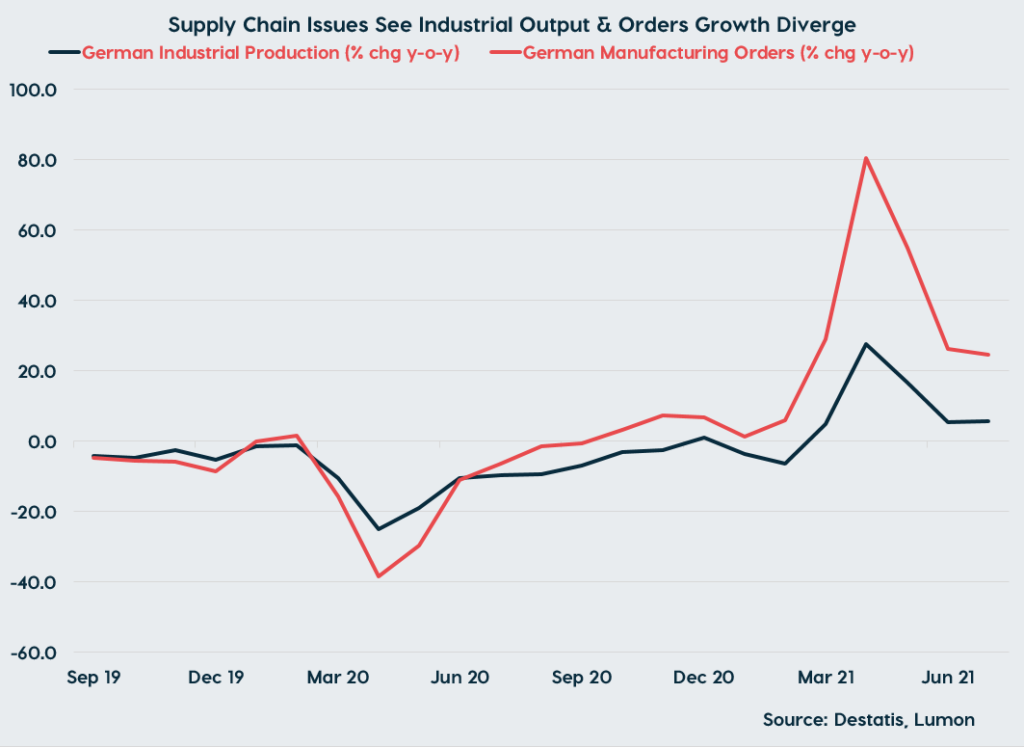

Euro

The euro largely range-traded yesterday, with GBP/EUR holding close to the €1.165 mark. Data-wise, it was confirmed yesterday morning that German industrial orders rose by 3.4% m-o-m in July, well above consensus forecasts for a 1% fall. Encouragingly, the fall was driven by a sharp rise in orders for ships, as freight companies seek to boost capacity. The issue, however, is that owing to the persistence of supply chain disruptions that in turn are a function of transportation bottlenecks, German manufacturers are struggling to source the materials needed to build these boats (and industrial products more generally). That said, industrial output did rise by a solid 1.0% in July, though this still left total production some 5.5% below February 2020 levels as the auto sector in particularly has been held back by a significant shortages of semiconductors.

Turning to the day ahead, there isn’t too much out to influence the euro. Something that is worth flagging, however, is that the EU appears to have softened their stance on the implementation of the Northern Ireland protocol, reducing near-term downside risks for GBP/EUR. Reports have suggested that the EU will not trigger legal action if the UK unilaterally extends a grace period that is due to end on September 30 under which the introduction of checks on goods trade between Great Britain and NI have been delayed. That said, a longer-term solution is still lacking, with the EU continuing to guide that it will not reopen trade talks with UK that were concluded only last December.

Sterling

Sterling was again lacking any fundamental drivers yesterday and struggled for direction as a result. The currency has been little impacted by chatter over the Conservative government’s social care reforms and a modest increase in the NHS budget, with the former expected to be funded via an increase in National Insurance rates. Concrete details of the plans will emerge today, when Prime Minister Johnson will present them to cabinet. While a return to austerity does not appear to be on the cards, the relative fiscal hawkishness of the Conservative government stands out as a possible headwind to sterling in the months ahead.

Meanwhile, reports suggested there was a significant increase in road traffic and public transport usage yesterday morning as schools reopened and on the back of return to the office mandates. This in turn implies we may see an uptick in economic activity in September, though the big caveat remains the trajectory of the pandemic. Cases are continuing to grind higher, while hospitalisations are up at end-February even before the impact from increased mobility levels has fed through.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).