Dollar

The dollar remained reasonably well-supported yesterday, with GBP/USD opening this morning at the midpoint of the $1.36-1.37 band and EUR/USD continuing to trade in the lower half of the $1.17-1.18 range. Investor sentiment has generally remained fragile over the past 24 hours, as we saw the boost from ‘Turnaround Tuesday’ evident in the European session fade as we approached the US close. We remain of the view that we are not on the cusp of a pronounced sell-off on financial markets but note that an improvement in risk appetite may not come until the event risk associated with tonight’s Federal Reserve (Fed) monetary policy meeting has cleared.

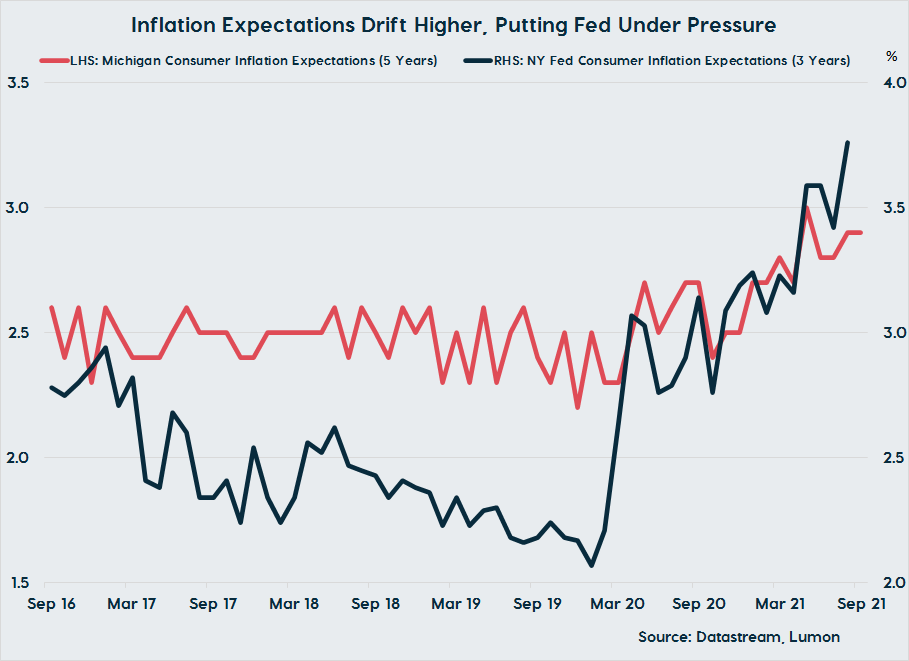

No changes to the policy are anticipated, with the fed funds rate to be held in its 0.00-0.25% range and a decision on tapering the central bank’s asset purchase programme likely to be delayed until Q4. There had initially been some speculation that an announcement in this regard could be made today, but some softer than anticipated inflation data and a weak August employment reported has pushed the timeline back. Granted, the central bank will be somewhat concerned that household inflation expectations are continuing to edge higher, while strong earnings growth suggests that the labour market may be tighter than the headline unemployment rate suggests. However, these developments are at an early stage, and we haven’t seen sufficient FOMC members voice concerns on this front that would indicate a tapering decision was imminent.

In terms of the meeting materials, attention will be firmly focused on the latest ‘dot plot’, which shows where Fed officials expect the funds rate to be in the coming years conditioned on their macro forecasts. The release of the last iteration in June saw the dollar rally significantly as most officials signalled for the first time that they saw a case for interest rate hikes in 2023. There is some speculation that most policymakers may now make the case for the tightening cycle to begin as early as next year, and such a move would certainly be consistent with a firming of the dollar tonight. That said, our base is for no changes to be made to the dots given the soft labour market / inflation figures and signs that economic growth is beginning to ease as the pandemic persists.

Sterling

Sterling will again take its cue from developments in risk appetite today, with a move in GBP/EUR back above the €1.17 threshold unlikely until we see a pronounced rebound in sentiment. On the data front, the schedule remains quiet ahead of tomorrow’s release of the flash September PMIs and Bank of England (BoE) policy announcement. With respect to the latter, it is worth noting that a YouGov survey released yesterday showed a recorded jump in inflation expectations in September, indicating that expectations are gradually becoming de-anchored from the central bank’s 2% target.

Euro

Over in the eurozone, there is little out to provide direction to the single market currency at present. As a result, we could be in for another session of range-trading, as the euro continues to weather the latest bout of risk aversion reasonably well.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).