Sterling

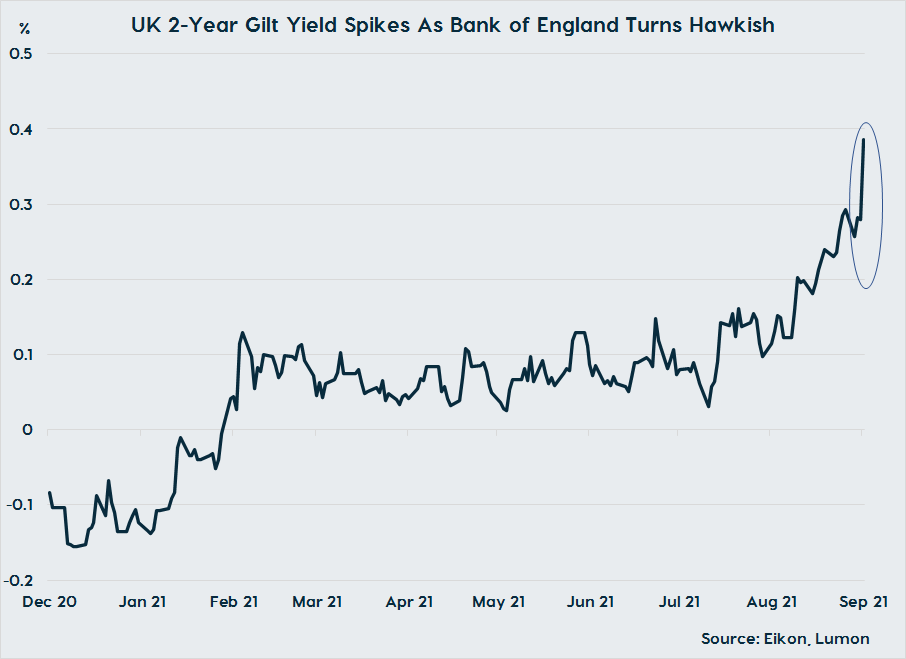

In line with our expectations, sterling saw strong support yesterday with GBP/USD breaking back up into the $1.37-1.38 band and GBP/EUR trading back up to the €1.17 level. This reflected a marked improvement in risk appetite that we had guided was on the cards once the event risk associated with Wednesday’s Fed meeting was out of the way. A further tailwind came from the relatively hawkish outcome of yesterday’s BoE meeting. Granted no changes to the policy were made (though 2 officials voted to prematurely end the central bank’s asset purchase programme, up from one in August) and the central bank did guide that growth would disappoint relative to expectations as supply chain issues bite.

Importantly, however, the BoE is becoming concerned about the possibility of runaway inflation (now sees the year-on-year rate peaking at over 4% in Q4), with developments in this regard since its last meeting in August strengthening the case for monetary policy tightening per the meeting minutes. Buried in the minutes was also an acknowledgement that rate hikes need not wait until the central bank’s asset purchase programme has concluded, which arguably opens the door to an increase in the Bank Rate from its current low of 0.10% at the November policy meeting. We view this risk as limited for now, given our belief that the central bank will want to delay acting until more evidence on the impact of the end of furlough this month has on labour markets is available and there is greater certainty surrounding the trajectory of the pandemic.

We do, though, see scope for a 0.15% interest rate hike at the February 2022 policy meeting, assuming we do not see a notable deterioration in the epidemiological situation, given price pressures are building and we are seeing a fairly pronounced uptick in inflation expectations, which is already of some concern to several MPC officials. Such a move would be in line with market pricing, with traders moving to price in a 15bps hike in February and an additional 25bps hike in August in the aftermath of yesterday’s meeting. This in turn should offer decent support to sterling, though the prospect of stagflation (slowing growth & higher inflation) in the winter months may offset some of the upside for the UK currency. Yesterday, brought news that BP will begin to ration petrol as driver shortages mean it can’t meet delivery requirements, while the flash PMIs for September (a measure of business activity) were consistent with a recovery that is being held back by supply chain problems.

Dollar

In the US, the dollar did come off the boil slightly over the past 24 hours as sentiment improved, which saw EUR/USD push back toward the midpoint of the $1.17-1.18 range. We see scope for the greenback to remain on the back foot in the coming days as markets generally remain in risk-on mode, with little on the US calendar to influence the currency until the release of the September employment report on October 8.

Euro

Over in the eurozone, the single market currency struggled for direction yesterday and indications are that it will be more of the same today. As elsewhere, flash September PMIs printed on the soft side as catch-up effects continue to fade and the persistence of supply chain disruptions has acted as a major drag. In addition to these factors, we anticipate that growth in the eurozone will be further held back in the coming months by softening external demand as China undergoes a slowdown, weighing on the euro.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).