Euro

The euro remained on the back foot yesterday, with EUR/USD holding in the lower half of the $1.18-1.19 threshold and GBP/EUR popping above the €1.17 threshold. The single market currency failed to find support from the conclusion of the ECB’s policy meeting. This was despite the central bank announcing that it would buy bonds under the Pandemic Emergence Programme at a “moderately slower pace” than in Q2 and Q3. This was a move that was framed as a ‘recalibration’ rather than a taper. We note that President Lagarde’s comments were not notably dovish. Indeed, she indicated during the press conference that while current elevated inflation (3% y-o-y in August) is likely to prove transitory, the central bank is aware that supply chain disruptions may prove more persistent than anticipated and is closely watching for second-order effects on wage inflation.

Attention will now turn to the ECB’s December meeting when Lagarde indicated that a decision will be made on the central bank’s bond-buying activities in 2022. We anticipate that the €1.85trn Pandemic Emergency Purchase Programme (PEPP) will be allowed to expire as planned in March 2022, but this will be compensated for via an increase in purchases under the ECB’s standard Asset Purchase Programme. However, the actual policy decision will be conditioned on incoming eurozone macroeconomic data, with inflation figures unsurprisingly set to attract significant attention. Against this uncertain backdrop, a close eye will be kept on central bankers’ comments, with Lagarde due to speak today. That said, we would be surprised if she offered much in the way of policy insights, meaning the single market currency could remain slightly on the back foot today.

Sterling

Sterling saw good support yesterday, with GBP/USD bouncing from a low of $1.375 up toward the midpoint of the $1.38-1.39 band. There was no obvious catalyst for this move, though the initial sell-off earlier in the week was lacking a macro driver, to begin with. Markets generally remained in risk-off mode, with equities coming under some further marginal downward pressure, while the UK macro schedule had a relatively uninspiring look to it. The highlight was the latest set of official furlough figures from HMRC, though these were if anything slightly disappointing. Despite the lifting of remaining Covid restrictions on July 16, the percentage of the workforce enrolled on the Job Retention Scheme edged only marginally lower from 5.8% to 5.4%.

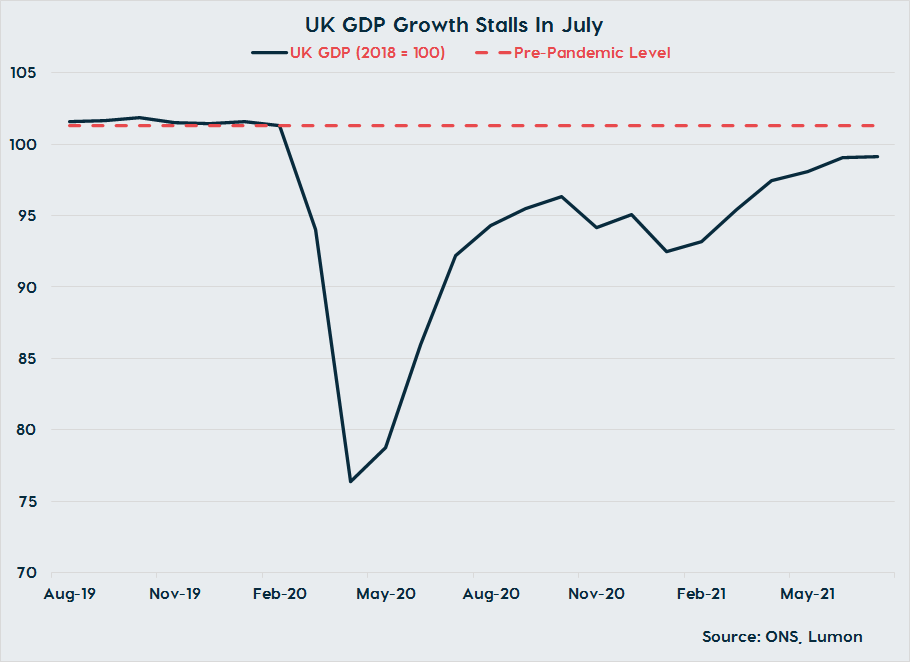

This morning, UK GDP figures for July were also printed on the soft side, though the impact on sterling was negligible given the lagging nature of the data and the fact that the forecast range was very wide. As the ‘pingdemic’ hit in the month, growth slowed markedly and the economy expanded by just 0.1% despite the economy mostly re-opening around mid-month. Higher frequency indicators suggested that momentum was regained in August and that a rise in mobility levels will act as a tailwind in September, but the recovery is clearly being held back by the persistence of the pandemic and significant supply chain issues. In terms of the day ahead, we anticipate that sterling will take its cue from developments in risk appetite.

Dollar

The dollar generally struggled for direction yesterday, with the macro schedule today unlikely to influence the action. The highlight is the August print of producer price inflation, which is likely to point to a further sharp increase in firms’ costs in the month on the back of severe supply chain disruptions. However, the data is typically not a mover for markets, as it has a limited relationship with consumer price inflation which is what the Fed targets.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).