Dollar

The dollar made some modest gains yesterday, with GBP/USD falling back into the lower half of the $1.37-1.38 range and EUR/USD dropping down to the $1.18 threshold. The action in part appeared to be a function of month-end flows, with the greenback at first rallying into the London fixing at 4pm UK time. Data-wise, the docket brought the release of further soft US macro-economic figures, with the Conference Board measure of consumer confidence plunging to February levels in August on the back of concerns surrounding elevated inflation and the spread of the delta variant. The data affirmed the message from the University of Michigan measure, suggesting that momentum in consumer spending growth has been lost in August after a strong H121. While we remain of the view that activity will pick back up as the pandemic recedes, recent figures from Israel pointing to waning immunity six months after vaccination are clouding the outlook.

Today will bring the publication of the manufacturing ISM (a measure of business activity) for August, with regional PMI data suggesting that output was again held back by supply chain disruptions in the month. New orders growth is also likely to have slowed, in keeping with the trend seen elsewhere suggesting that the global manufacturing cycle may have peaked. In addition to the ISMs, the ADP estimate of private payroll growth for August may also attract some attention, though we note that it has historically been a poor predictor of the official non-farm payroll figure. Overall, the data should offer an unhelpful backdrop for the dollar, though we note that markets have tended to ignore soft US macro-economic data in recent months.

Euro

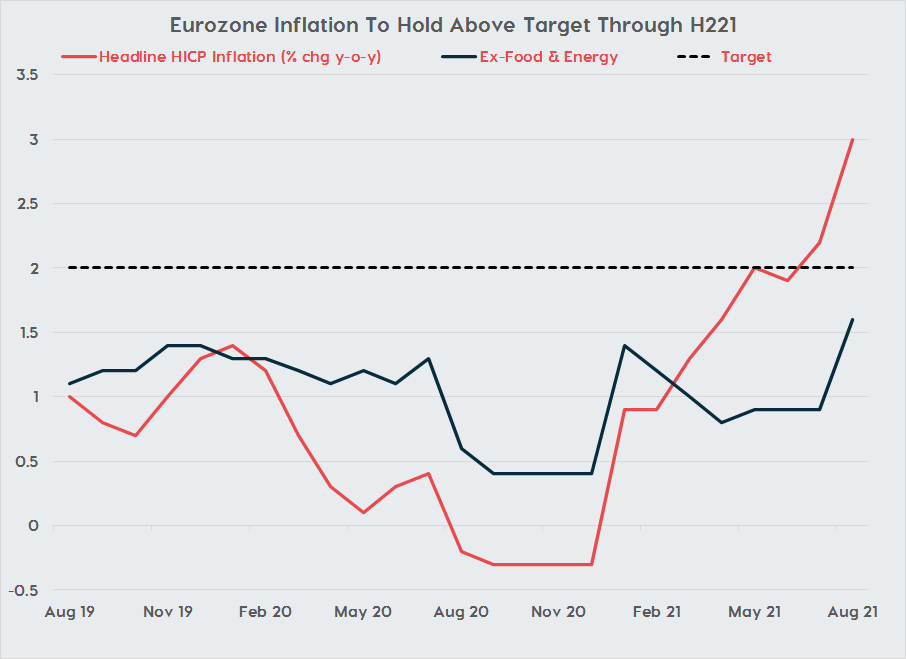

There were several interesting developments in the eurozone yesterday, which saw GBP/EUR drift into the lower half of the €1.16-1.17 band. First, we saw eurozone headline inflation print at a 10-year high of 3.0% year-on-year (forecast: 2.7%), while the core rate (ex-food & energy) jumped from 0.9% to 1.6% (forecast 1.4%). This was then followed by a series of comments from ECB hawks, with several officials hinting heavily that there is a non-negligible risk that the central bank’s asset purchase programme will be tapered before year-end. The combined impact from these events saw eurozone bond yields soar, with Italian 10-year yields jumping by 10bps to a six-week high near 0.71%.

We remain sceptical, however, that these moves will be sustained and expect that ECB policy will remain highlight accommodative in the years to come. Indeed, the reaction in fixed income markets to the latest headlines will already likely be of some concern to officials, with the central bank keen to avoid a mini-taper tantrum. Moreover, even if the ECB does cut back on the pace of its asset purchases, it has emphasised that new purchases will not come to a halt as the central bank attempts to maintain favourable financial conditions. Weak underlying price pressures linked to persistently high unemployment back this stance, with yesterday’s apparent jump in inflation a by-product of the reversal of temporary tax cuts, a rebound in global energy prices and the timing of sales. We note, however, that it may take for this narrative to re-assert itself on financial markets

Sterling

Another quiet day lies ahead for sterling, with the macro schedule providing little in the way of direction. Yesterday, the Lloyds Business Barometer suggested that business confidence rose to a 4-year high in August on the back of re-opening effects and the end of the ‘pingdemic’. Our base case remains that UK growth will remain solid in the coming months, though we are increasingly concerned that a jump in Covid cases in the coming weeks could dent the recovery as we head into the winter, limiting the upside for sterling.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).