Euro

The euro has remained reasonably well supported over the past 24 hours, with GBP/EUR pushing down into the lower half of the €1.16-1.17 and EUR/USD continuing to test resistance near the midpoint of the $1.18-1.19 band. A weak German retail sales print for July released yesterday morning (-5.1% month-on-month vs forecast –0.9%) had no impact on the single market currency, reflecting the fact that the data are often volatile and in any case the softness can be at least partly explained by a switch from goods to services expenditure as the economy has reopened.

Turning to the day ahead, there is little out to provide influence on the euro. The macro schedule is barren, while the ECB has entered its quiet period ahead of next week’s policy meeting. Overall, we anticipate that the currency will remain reasonably well supported in the lead-up to this event as the market continues to toy with the possibility of the central bank announcing a modest reduction in the pace of its monthly bond purchases. While we do not rule out such an outcome, we are inclined to believe that the Governing Council will opt to remain on hold until December, when it will have more clarity on the trajectory of the pandemic and will have had more time to prepare investors for such a policy shift, reducing the risk of a mini taper tantrum.

Dollar

The dollar came under some slight downward pressure yesterday, though its main pairs remained well within recent trading ranges as GBP/USD again struggled to break through the $1.38 threshold.

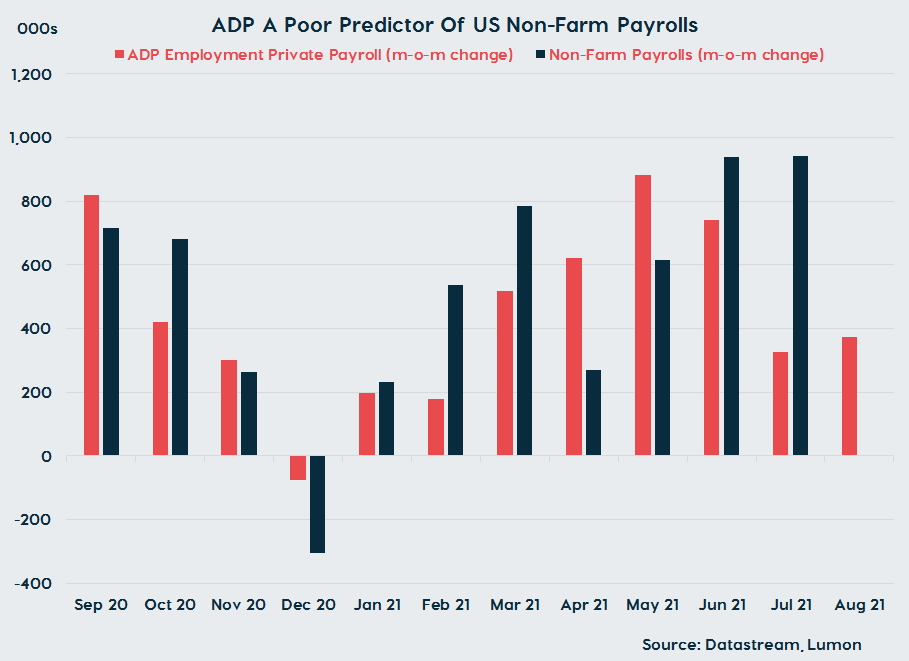

The emergence of modest greenback softness coincided with a rebound in investor risk appetite on this side of the Atlantic and a weak reading of the ADP’s private payroll report for August. The latter suggested just 374k jobs were created in the month, suggesting we may be in store for a weak employment report on Friday. However, as we have previously highlighted, the ADP is a remarkably poor predictor of the official non-farm payroll figure, and we continue to question why the data attract the attention of dollar watchers.

Meanwhile, the manufacturing ISM came in surprisingly strong in August, pushing up to 59.9 from 59.5. The data indicated that activity in the sector increased in the month, with new orders growth also picking up. However, supply chain issues remain a major headwind, while businesses are struggling to retain and attract workers (bodes poorly for payrolls on Friday). Overall, we remain of the view that the global manufacturing cycle has peaked, though strong demand will see growth remain solid in the medium-term.

Looking to the day ahead, there is a subdued look to the macro schedule, meaning fundamentals won’t be a major driver of the action. In terms of sentiment, Asian equities were mixed overnight, suggesting that the greenback could retain some support over the next 24 hours.

Sterling

The UK calendar is again devoid of any market moving releases today, with the action in sterling set to be driven by the other half of its main pairs as a result. There was some positive news on the Covid front yesterday, with the latest set of daily figures showing cases decreased on a week-on-week basis. However, the experience from Scotland suggests that infections are likely to rise again in the coming weeks as schools return, with universities to follow.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).