Dollar

The dollar saw some support following yesterday’s Fed meeting, with GBP/USD holding in the lower half of the $1.36-1.37 range and EUR/USD testing below $1.17. Markets treated the outcome as slightly hawkish, though in our view it was something of a non-event. As anticipated, a decision on tapering the central bank’s asset purchase was not made. However, it appears overwhelmingly likely that the announcement will come in November unless we see a marked deterioration in economic conditions between now and this date. Interestingly, Chair Powell signalled in the press conference that the tapering process should be completed by mid-year 2022.

This suggests that we could see the central bank move to hike rates by the end of 2022, though the updated ‘dotplot’, which shows policymakers’ projections for the fed funds rate conditioned on their macroeconomic forecasts, indicates that officials are split on this question. Looking beyond 2022, officials now anticipate there will be three interest rates hikes by the end of 2023 (previously two), with just one FOMC member now expecting the central bank to remain on hold through this horizon.

Our view is that the tightening cycle will begin by the end of Q422, which is roughly in line with what money markets are pricing. This reflects our belief that US inflation will remain well above the central bank’s 2% target over the next 15 months, with tightening labour market conditions generating strong underlying price pressures, even as transitory factors linked to supply chain issues and spiking energy prices begin to fade. This will in turn keep the dollar reasonably well-supported over the next year, though in the more immediate future we anticipate that the greenback will move off its highs given that yesterday’s meeting was not overly hawkish and as risk appetite has continued to rebound.

Sterling

Today, it is the turn of the Bank of England to hold its policy meeting, which we believe poses some upside risk for sterling and could see GBP/EUR trade back toward €1.17. BoE policymakers sounded notably hawkish when they appeared before the Treasury Select Committee as they signalled their concern that labour market shortages may be structural rather than cyclical (linked to a decline in the labour force participation rate and declining immigration), a factor that could see earnings growth pick up notably in the coming quarters.

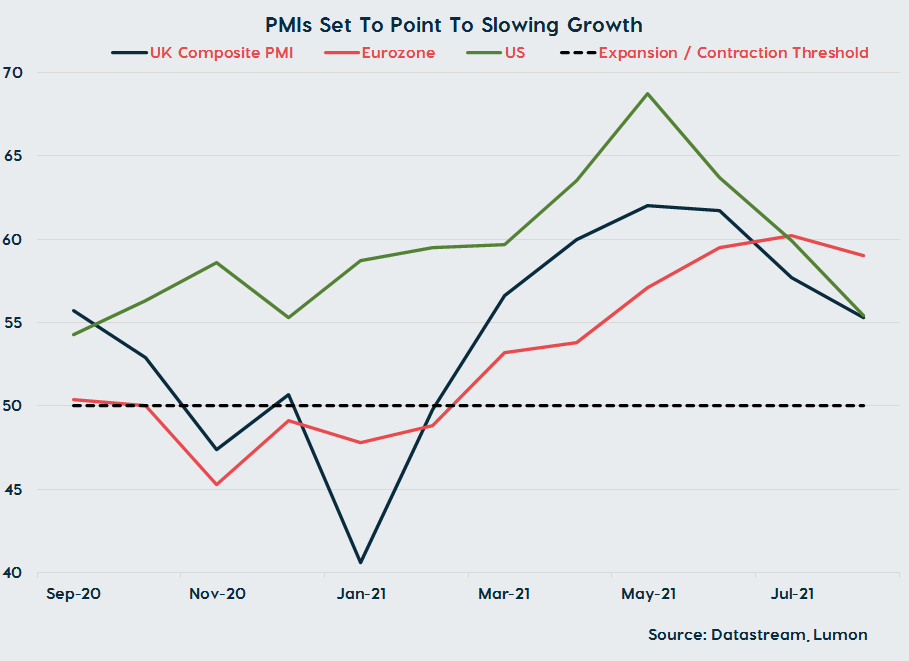

This comes at a time when price pressures are already elevated, reflecting significant supply-side issues (spiking electricity prices, new Brexit restrictions and transportation bottlenecks). There are some concerns that inflation expectations are becoming de-anchored from the BoE’s 2% target and given this backdrop, we do see some scope for an increased number of MPC members to signal their support for ending purchases under the central bank’s QE programme immediately rather than waiting until the end of the year as planned (just one committee member voted for this in August). This should provide support for sterling, given it would arguably set the scene for earlier interest rate hikes. It is also worth noting that the UK flash PMIs for September are also due today, which are a bit of a wildcard given their relationship with actual economic activity has deteriorated, but pose some event risk for sterling.

Euro

Over in the eurozone, the focus will be on the flash September PMIs that are also due this morning. We anticipate that the data will continue to point to easing growth in the region as catch-up effects following the easing of lockdown fade, which could provide some modest downside risk to the single market currency.

This blog post is intended to provide you with information on the services Lumon Pay Ltd (“LPL”) offer and should not be interpreted as advice or as a solicitation to offer to buy or sell any currency or as a recommendation to trade. Foreign exchange rates provided therein are for indicative purposes only and are not intended to give an accurate reflection of current currency exchange rates or to predict future movements in currency exchange rates. LPL, trading as Lumon, is a company registered in England with its registered address at Building 1, Chalfont Park, Gerrards Cross, Buckinghamshire SL9 0BG. LPL is authorised by the Financial Conduct Authority as an Electronic Money Institution (FRN: 902022).